inancial Risks Insurance Can Help Reduce Key Takeaways

Every day, families and professionals face unexpected expenses that can derail even the most careful budget.

- Financial Risks Insurance Can Help Reduce include emergency medical expenses, income loss, property damage, and liability claims — each covered by a specific policy type.

- health insurance and disability insurance protect against medical and income shocks, while life insurance safeguards dependents from debt and loss of future earnings.

- Comprehensive insurance protection is a cornerstone of wealth preservation , preventing forced asset liquidation and supporting long-term financial stability .

Understanding the Role of Insurance in Reducing Financial Uncertainty

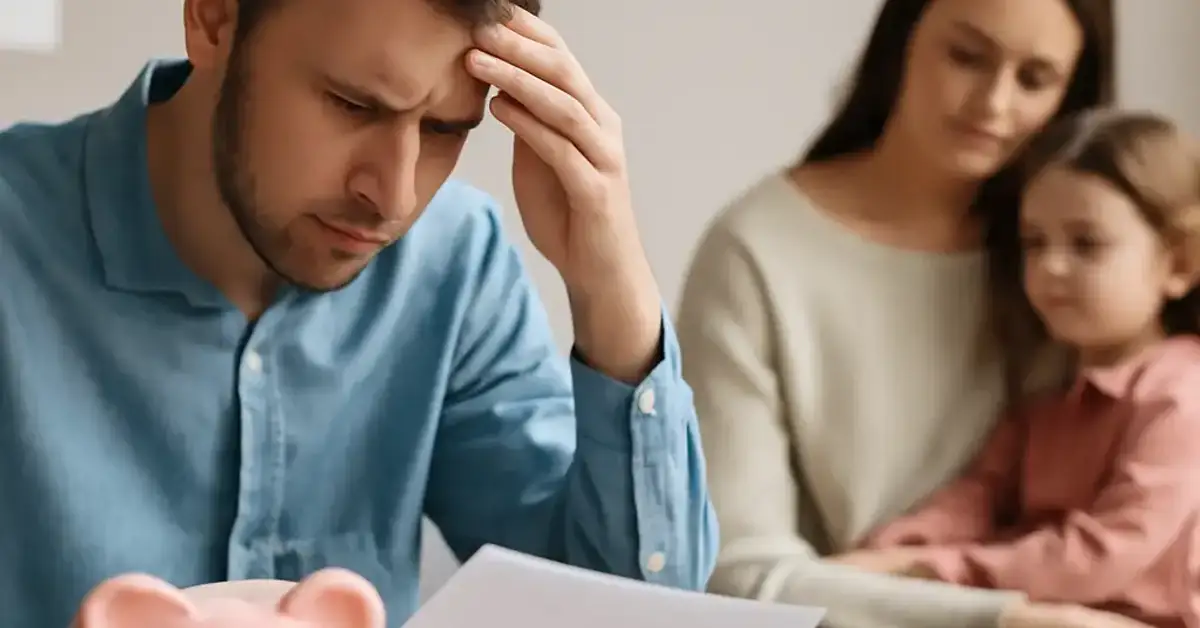

Every day, families and professionals face unexpected expenses that can derail even the most careful budget. A medical emergency, a car accident, a lawsuit, or a sudden disability — each event carries a price tag that can wipe out years of savings. That is precisely where Financial Risks Insurance Can Help Reduce the gap between a manageable setback and a financial catastrophe. By transferring the burden of large, unpredictable losses to an insurer, you gain financial security and peace of mind.

Why Risk Transfer Matters for Personal Finance

Insurance is, at its core, a risk mitigation tool. Instead of bearing the full cost of a major loss alone, you pay a predictable premium. That premium buys you insurance coverage that steps in when you need it most. For young professionals, freelancers, OFWs, and business owners, this mechanism is essential for protecting personal finance goals like homeownership, retirement, and education funding.

1. Unexpected Medical Expenses and Hospitalization Costs

how insurance protects against unexpected medical expenses and hospitalization costs is one of the most immediate benefits people experience. A single emergency room visit can cost thousands of dollars; a surgery can exceed tens of thousands. Without coverage, those costs often lead to credit card debt, loans, or even bankruptcy. For a related guide, see How to Compare Insurance Policies Beyond Premium Costs.

health insurance policies — whether employer-sponsored or individual — cover hospital stays, surgeries, diagnostic tests, and prescription drugs. Some plans also include preventive care, which reduces the likelihood of expensive emergencies later. For Filipinos working abroad (OFWs) and families back home, having reliable coverage means that a sudden illness does not drain the family’s savings.

How does insurance reduce the financial impact of an emergency hospital stay? It negotiates discounted rates with hospitals and pays a portion (often 80–100%) after you meet your deductible. This insurance protection ensures that one medical event does not become a lifelong debt trap.

2. Risk of Income Loss Due to Disability or Illness

risk of income loss due to disability or illness and how insurance provides income protection is a critical concern for anyone who relies on a paycheck. If you cannot work for six months or two years due to an injury, chronic illness, or mental health condition, your mortgage, utilities, and daily expenses continue. disability insurance replaces a portion of your income — typically 60–70% — during that period.

This type of income protection is especially important for freelancers, entrepreneurs, and gig workers who lack employer-paid sick leave. By paying a monthly premium, you secure a safety net that keeps your family afloat and prevents you from draining your emergency fund or retirement accounts. insurance benefits like own-occupation coverage ensure that you are covered even if you can no longer perform your specific job.

How does disability insurance protect earning capacity? It offers both short-term and long-term benefits. Short-term policies cover the initial weeks or months; long-term policies extend for years or until retirement age. Together, they provide financial resilience during a health crisis.

3. Financial Impact of Accidents and Emergency Medical Situations

financial impact of accidents and emergency medical situations goes beyond hospital bills. Lost wages, rehabilitation costs, home modifications, and transportation expenses add up quickly. Accident insurance and personal accident coverage are designed to address these gaps.

Unlike comprehensive health insurance, accident insurance pays a lump sum or a fixed benefit per incident. This cash can be used however you need — whether to cover your rent, hire a caregiver, or pay for therapy. For active families, young professionals, and employees in manual labor industries, this coverage provides an extra layer of financial security.

How does accident insurance reduce stress during recovery? By providing quick, tax-free cash, it removes the financial pressure so you can focus on healing. That is a key part of risk mitigation for emergency expenses.

4. Protection Against High Out-of-Pocket Costs from Critical Illnesses

protection against high out-of-pocket costs from critical illnesses is a major reason people invest in specialized policies. Cancer, heart attacks, strokes, and kidney failure require expensive treatments that ongoing care can exhaust even generous health insurance plans.

Critical illness insurance pays a one-time, lump-sum benefit upon diagnosis of a covered condition. That money can cover deductibles, experimental treatments, travel to specialists, or lost income while you undergo treatment. For breadwinners and families, this insurance coverage prevents a medical crisis from becoming a financial tragedy. For a related guide, see 8 Situations That May Require Additional Coverage.

Why is critical illness insurance becoming more popular in the Philippines and Southeast Asia? Because healthcare costs are rising faster than general inflation. A lump-sum benefit helps families preserve their savings and emergency funds while accessing the best care available.

5. How Life Insurance Reduces Financial Burden on Dependents

how life insurance reduces financial burden on dependents is one of the most well-understood roles of insurance. When a primary earner passes away, surviving family members lose not only emotional support but also future income. life insurance provides a tax-free payout that can replace years of earnings, pay off a mortgage, fund education, and cover daily living expenses.

Term life insurance is affordable for young professionals and families, offering high coverage amounts for a fixed period (e.g., 20 years). Whole life or universal life policies add a cash value component, which can serve as a savings vehicle over time. For OFWs who support parents and siblings back home, life insurance is the ultimate asset protection tool: it ensures that your family’s standard of living continues even in your absence.

How does life insurance prevent forced asset liquidation? Without a payout, grieving families may need to sell property, cars, or investments to cover funeral costs and ongoing bills. Life insurance cash replaces that need, preserving the wealth preservation you built.

6. Coverage for Property Damage and Asset Loss Risks

coverage for property damage and asset loss risks protects the physical belongings you work hard to acquire. Your home, car, business equipment, and personal valuables are exposed to fire, theft, storms, floods, and other perils. property insurance — including homeowners, renters, and auto policies — reimburses you for repair or replacement costs.

For business owners, property coverage extends to inventory, machinery, and office space. Without it, a single fire or typhoon can halt operations and cause irreparable financial stability damage. insurance protection for property is a non-negotiable part of risk management for anyone who owns assets.

What types of property insurance do families need most? Homeowners or renters insurance for the dwelling and contents, plus comprehensive car insurance. For business owners, a commercial property policy that includes business interruption riders is essential.

7. Protection Against Legal Liability and Third-Party Claims

protection against legal liability and third-party claims is often overlooked until a lawsuit arises. If someone gets injured on your property, you cause a car accident, or your business inadvertently harms a client, you could be held financially responsible for medical bills, legal fees, and damages. liability insurance covers these costs.

General liability policies are standard for businesses, while personal liability is included in homeowners and auto policies. Umbrella insurance provides an extra layer of coverage above your primary policies. For high-net-worth individuals, professionals (doctors, lawyers, consultants), and property owners, liability protection is essential for financial security.

How does liability insurance reduce the risk of losing everything in a lawsuit? Legal defense alone can cost tens of thousands — before any settlement. Liability policies pay for defense and covered judgments, protecting your savings, property, and future earnings.

8. Role of Insurance in Reducing Debt-Related Financial Stress During Emergencies

role of insurance in reducing debt-related financial stress during emergencies is a vital but underappreciated benefit. When a medical crisis, accident, or job loss strikes, many people turn to credit cards, personal loans, or payday lenders to cover immediate needs. These high-interest debts compound the original problem. Insurance breaks that cycle by providing cash directly.

For example, disability insurance income replaces income so you keep paying your mortgage. health insurance pays hospital bills before they go to collections. Critical illness and accident insurance give lump sums that cover deductibles and living expenses. By reducing the need to borrow, insurance reduces debt-related financial stress and protects your credit score.

How does insurance support financial resilience during job loss or health crises? It ensures that your only focus is recovery — not how to make next month’s rent. That is the core of financial stability.

9. How Insurance Helps Manage Business Interruption and Loss of Income for Entrepreneurs

how insurance helps manage business interruption and loss of income for entrepreneurs is a game-changer for small business owners. A natural disaster, fire, equipment failure, or even a pandemic can shut down operations for weeks or months. During that time, fixed costs — rent, salaries, loan payments — continue. Business interruption insurance replaces lost revenue until you reopen.

For freelancers and digital marketers, similar coverage can protect against client loss, technology failures, or professional liability claims. insurance benefits tailored to business risk ensure that one setback does not force you to close for good.

What coverage do entrepreneurs need most? A business owner’s policy (BOP) that bundles property, liability, and business interruption. Freelancers should consider professional liability (errors and omissions) and disability insurance as well.

10. Protection Against Rising Healthcare Costs and Inflation-Related Expenses

protection against rising healthcare costs and inflation-related expenses is becoming more urgent every year. Medical inflation often outpaces general inflation by 2–3 times. Hospital room rates, surgery costs, and prescription drug prices escalate quickly. Without adequate coverage, even routine care becomes a burden.

health insurance plans with guaranteed renewability, capped out-of-pocket maximums, and inflation-adjusted benefits help you stay ahead. Some life insurance and critical illness insurance policies include riders that increase coverage amounts with inflation. This risk mitigation approach ensures that your insurance coverage does not lose value over time.

How does inflation affect my insurance needs? A policy bought ten years ago might be insufficient today. Annual reviews and indexed benefits help maintain financial security in the face of rising prices.

Useful Resources

For further reading on risk management and financial planning, consider these credible sources:

- Investopedia – Insurance Basics: How to Protect Your Finances

- NerdWallet – Health Insurance Guide for Individuals and Families

Conclusion: Building a Resilient Financial Future with Insurance

Understanding the 10 core areas where Financial Risks Insurance Can Help Reduce is the first step toward a stronger financial planning strategy. From health insurance covering hospital bills to life insurance protecting your loved ones, each policy plays a specific role in risk management. For young professionals, families, OFWs, freelancers, and business owners, comprehensive insurance coverage is not an expense — it is an investment in wealth preservation and financial stability.

Start by evaluating your personal risk exposure: Do you have dependents? Do you own a home? Do you work in a physically demanding job? Then match that exposure with the right mix of policies. The premiums you pay today are a small price for the protection you gain — and the peace of mind that comes from knowing that Financial Risks Insurance Can Help Reduce even the biggest surprises.

Frequently Asked Questions About Financial Risks Insurance Can Help Reduce

What are the most common financial risks that insurance can help reduce?

The most common financial risks include unexpected medical expenses, income loss due to disability or illness, property damage, liability claims, and premature death. Financial Risks Insurance Can Help Reduce each of these by providing financial payouts or direct payment for covered events.

How insurance protects against unexpected medical expenses and hospitalization costs ?

health insurance covers hospital stays, surgeries, doctor visits, and prescriptions. After you meet your deductible, the insurer pays a percentage of covered costs, protecting you from massive out-of-pocket bills. This is a primary example of how insurance protects against unexpected medical expenses and hospitalization costs.

What is the risk of income loss due to disability or illness and how insurance provides income protection ?

disability insurance replaces a portion of your income — usually 60–70% — when you cannot work due to illness or injury. This income protection covers ongoing expenses like rent, utilities, and food, preventing you from falling into debt.

How does insurance reduce the financial impact of accidents and emergency situations?

Accident insurance pays a lump sum or fixed benefit per incident, which you can use for medical deductibles, lost wages, or home modifications. This insurance coverage directly addresses the financial impact of accidents and emergency medical situations.

What is protection against high out-of-pocket costs from critical illnesses ?

Critical illness insurance pays a lump sum upon diagnosis of a covered condition like cancer, heart attack, or stroke. This protection against high out-of-pocket costs from critical illnesses helps pay for deductibles, experimental treatments, and lost income.

How life insurance reduces financial burden on dependents ?

life insurance provides a tax-free payout to beneficiaries upon your death. This cash can replace lost income, pay off debts, fund education, and cover funeral costs. This is exactly how life insurance reduces financial burden on dependents.

What is coverage for property damage and asset loss risks ?

property insurance — including homeowners, renters, and auto policies — reimburses you for repair or replacement costs after covered perils like fire, theft, or storm. This coverage for property damage and asset loss risks protects your physical assets.

How does insurance protect against legal liability and third-party claims?

liability insurance covers legal defense fees, medical bills, and damages if someone is injured on your property or you cause an accident. This protection against legal liability and third-party claims prevents lawsuits from wiping out your savings.

What is the role of insurance in reducing debt-related financial stress during emergencies ?

By providing direct payouts for medical, disability, or property losses, insurance reduces your need to borrow money. This role of insurance in reducing debt-related financial stress during emergencies helps you avoid high-interest debt and preserve your credit.

How insurance helps manage business interruption and loss of income for entrepreneurs ?

Business interruption insurance replaces lost revenue when a disaster forces you to close temporarily. This is how insurance helps manage business interruption and loss of income for entrepreneurs, covering ongoing fixed costs like rent and salaries.

What is protection against rising healthcare costs and inflation-related expenses ?

Policies with guaranteed renewability and inflation-adjusted benefits help your coverage keep pace with medical inflation. This protection against rising healthcare costs and inflation-related expenses ensures your plan remains adequate over time.

What is the importance of insurance in safeguarding savings and emergency funds ?

Without insurance, a single medical emergency or accident can drain your entire emergency fund. The importance of insurance in safeguarding savings and emergency funds lies in its ability to cover big losses so your cash remains untouched.

How does insurance support risk mitigation for long-term financial planning stability ?

By capping your potential losses, insurance allows you to project expenses and savings more accurately. This risk mitigation for long-term financial planning stability helps you stick to investment and retirement goals without fear of a major setback.

How insurance reduces financial uncertainty in major life events ?

Marriage, having children, buying a home, and starting a business all come with increased risk. Proper insurance coverage reduces the financial shock if something goes wrong, providing financial security during transitions.

What is coverage for travel-related financial risks and emergencies ?

Travel insurance covers trip cancellations, lost luggage, medical evacuations, and emergency medical expenses abroad. This coverage for travel-related financial risks and emergencies is essential for OFWs, digital nomads, and frequent travelers.

What is the importance of disability insurance in protecting earning capacity ?

Your ability to earn an income is your most valuable asset. The importance of disability insurance in protecting earning capacity lies in its ability to replace a significant portion of your salary if you cannot work, keeping you financially stable.

How insurance supports financial resilience during job loss or health crises ?

disability insurance, health insurance, and critical illness coverage provide cash when you need it most. This how insurance supports financial resilience during job loss or health crises by ensuring you have income and medical benefits during tough times.

What is the role of insurance in avoiding forced asset liquidation ?

Without insurance, families often sell property, vehicles, or investments to pay for emergencies. The role of insurance in avoiding forced asset liquidation is to provide the cash needed to cover large expenses without selling assets at a loss.

How does insurance protect against catastrophic financial shocks?

Catastrophic events like a heart attack, a major car accident, or a house fire carry enormous costs. Insurance coverage limits your out-of-pocket exposure, providing protection against catastrophic financial shocks that would otherwise devastate your finances.

How insurance contributes to overall wealth preservation strategy ?

By preventing large, unplanned losses, insurance helps you keep your savings, investments, and property intact. This how insurance contributes to overall wealth preservation strategy is why financial advisors recommend it as a core part of any personal finance plan.