Underinsurance Can Be More Dangerous Key Takeaways

One of the biggest insurance mistakes people make is equating the presence of a policy with adequate protection.

- Underinsurance Can Be More Dangerous because it creates a false sense of security that prevents you from seeking proper protection.

- Partial payouts during emergencies still leave massive out-of-pocket expenses that can wipe out savings.

- Rising medical costs, inflation, and outdated coverage limits make insufficient coverage a ticking financial time bomb for families and individuals.

Why Underinsurance Can Be More Dangerous Than Having Zero Coverage

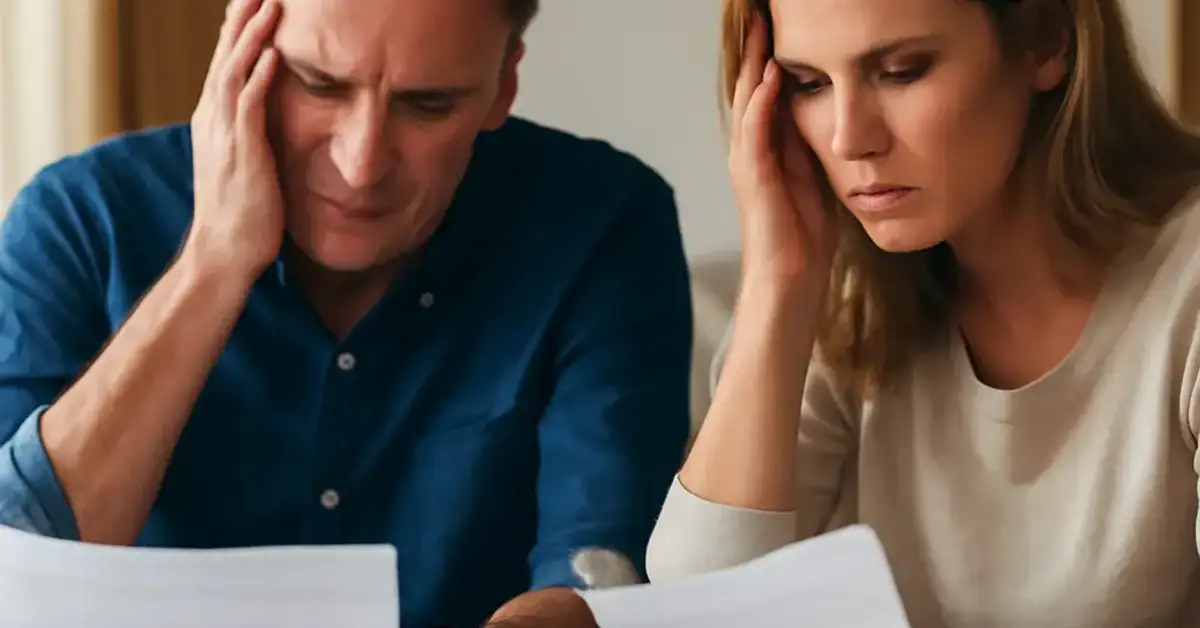

When you have no insurance coverage at all, you know exactly where you stand. You understand that any accident, illness, or property loss comes entirely out of your own pocket. That awareness drives careful behavior and forces you to build emergency funds. But underinsurance creates something far more insidious: a dangerous gap between what you believe is protected and what is actually covered.

The core problem lies in human psychology. Paying premiums month after month gives you a deep sense of financial security. You tick the box, file the paperwork, and assume you are safe. However, when a real emergency strikes, you discover your policy limits are too low, your deductibles are crushing, and critical gaps leave you exposed. This betrayal of trust carries an emotional and financial toll no one anticipates.

The False Sense of Security Trap

One of the biggest insurance mistakes people make is equating the presence of a policy with adequate protection. A family might buy a health plan thinking they are covered, only to face a $50,000 hospital bill because their annual maximum is too low. A homeowner might insure their house for its market value rather than replacement cost, finding themselves $100,000 short after a fire. These aren’t rare edge cases—they are everyday tragedies fueled by insufficient coverage. For a related guide, see Top Reasons Filipinos Buy Life Insurance Too Late.

The Hidden Financial Risks of Insufficient Coverage During Emergencies

When you face a real crisis, the financial structure of your policy matters more than anything else. The risks of insufficient coverage emergency situations are exposed in painful detail. You may face a claim denial for a covered event simply because your policy limits have been exhausted. Or worse, you may discover that sub-limits within your policy cap specific categories like water damage or temporary housing at fractions of the total coverage amount.

How Partial Payouts Still Leave Large Out-of-Pocket Expenses

Even when an insurance company pays a claim, the amount they pay may cover only a fraction of your actual loss. For example, a health insurance policy might pay 80% of a surgical procedure, leaving you responsible for the remaining 20%. That 20% on a $200,000 surgery is $40,000—enough to bankrupt many middle-income families. This is exactly why underinsurance more dangerous than no coverage becomes a harsh reality: you thought you were protected, but the financial devastation is nearly identical to having no policy at all.

The True Cost of Insurance Gaps When You Least Expect Them

Insurance gaps exist in every policy. They might be waiting periods, exclusions for pre-existing conditions, or limits on specific types of damage. For property insurance, gaps often appear in coverage for earthquakes, floods, or sewer backups—events that cause catastrophic emergency expenses. When these events happen, the difference between having full coverage and having insufficient coverage can be the difference between rebuilding your life and losing everything.

Underinsurance Life Insurance Dependents Face When Coverage Is Too Low

For families, life insurance is supposed to provide a safety net. Yet many policies are sized based on outdated formulas like “10 times your salary,” which fails to account for inflation, education costs, and long-term lifestyle needs. When a breadwinner dies, underinsurance life insurance dependents face a brutal reality. The payout might cover funeral expenses and a year of lost income, but it won’t fund college tuitions, pay off the mortgage, or support a spouse into retirement. The dependents are left in a financial hole that could have been avoided with proper financial planning.

The Emotional Toll of Insufficient Life Insurance

Beyond the numbers, inadequate life insurance adds profound emotional stress. A grieving spouse should not have to worry about selling the family home or pulling children out of school. Yet this is the direct result of insurance gaps in life coverage. The policyholder believed they had done the right thing, but their family pays the price for insufficient coverage at the worst possible time.

Health Insurance Coverage Gaps Medical Debt That Burdens Families for Years

The American healthcare system is expensive, and even those with employer-provided insurance face significant risks. Health insurance coverage gaps medical debt is one of the leading causes of bankruptcy in the United States. A sudden diagnosis, a car accident, or a chronic illness can quickly exhaust annual maximums, leaving families with hundreds of thousands in debt. The irony is that these individuals had insurance—they just didn’t have enough.

Impact of Rising Medical Costs on Underinsurance

Medical costs rise faster than general inflation every year. A health insurance policy that seemed generous five years ago may now be dangerously inadequate. Hospital stays, prescription drugs, and specialist visits cost significantly more than they did when you first signed up. Without regular insurance review, you are paying for protection that no longer fits reality. This is a classic example of why underinsurance is a dynamic risk, not a static problem.

Property Insurance Replacement Shortfall: When Your Home Isn’t Really Covered

Your home is likely your single largest asset. Yet many homeowners insure their property based on market value or purchase price, not the actual cost to rebuild. Property insurance replacement shortfall occurs when construction costs, material prices, and labor rates have risen since your policy was written. After a total loss, you might receive a check that covers only 70% of what it actually costs to rebuild. This gap can be hundreds of thousands of dollars for a family home.

The Reality of Minimum Coverage vs Adequate Coverage

The phrase “minimum coverage” should be a red flag for any insurance buyer. Minimum coverage meets legal requirements but rarely meets real-world needs. For auto insurance, state minimum liability limits are often laughably low compared to accident costs. For home insurance, minimum policies exclude replacement cost coverage. The difference between minimum coverage vs adequate coverage is the difference between paying a little more now versus facing financial ruin later.

Inflation Impact Insurance Planning in Ways Most People Ignore

Inflation is a silent destroyer of insurance coverage. It erodes the purchasing power of fixed benefit amounts over time. A $500,000 life insurance policy today will be worth significantly less in twenty years. A health insurance annual maximum of $1 million might seem high now, but if medical inflation continues at current rates, that limit could be exhausted quickly by a major illness. Inflation impact insurance planning must be a core part of every review cycle. For a related guide, see How Inflation Is Affecting Insurance Coverage Decisions.

How to Future-Proof Your Insurance Planning

The solution is not to buy minimum coverage and hope for the best. Instead, you should incorporate inflation adjusters, guaranteed purchase options, and regular policy reviews into your strategy. Risk management professionals recommend reviewing every policy at least every two years and adjusting coverage based on current costs, not past assumptions. This ensures your financial protection keeps pace with the real world.

Behavioral Mistakes Leading to Underinsured Decisions

Why do smart people end up with insufficient coverage? The answer lies in behavioral economics. People tend to underestimate the likelihood of rare but catastrophic events. They focus on the premium cost rather than the potential loss. They buy policies based on generic recommendations rather than personalized comprehensive risk assessment insurance planning. These behavioral biases are powerful, and they lead millions into the trap of underinsurance.

Employer-Provided Insurance: A False Safety Net

Many employees assume their workplace insurance is adequate. However, employer-provided health, life, and disability insurance is often designed as a basic benefit, not comprehensive protection. Group policies have lower limits, fewer options, and no personalization. Relying solely on employer insurance is one of the most common insurance mistakes people make. It leaves families exposed to insurance gaps that supplemental policies can easily fill. For a related guide, see 10 Insurance Gaps That Leave Families Financially Exposed.

How to Perform a Comprehensive Risk Assessment Insurance Check

Protecting yourself from the dangers of underinsurance starts with a thorough evaluation. Here is a practical checklist based on financial planning best practices:

- List all your assets and their current replacement costs.

- Calculate your total liabilities, including mortgages, loans, and future obligations.

- Review your current policy limits and compare them to actual risks.

- Check for sub-limits and exclusions that create insurance gaps.

- Adjust for inflation and rising costs in your region.

- Consider umbrella policies for additional liability coverage.

- Schedule an annual insurance review with a licensed advisor.

Using Data to Make Better Coverage Decisions

The days of guessing your insurance needs are over. Modern risk management tools allow you to calculate precise coverage amounts based on income, family size, debt, and future goals. A detailed comprehensive risk assessment insurance plan should include not just your current situation but projected future needs. This forward-thinking approach is the antidote to underinsurance.

The Long-Term Consequences of Inadequate Protection on Wealth Building

Underinsurance doesn’t just cause immediate financial pain; it sabotages long-term wealth. A single uncovered medical event can deplete retirement savings. An uninsured property loss can force you into debt that takes decades to repay. By protecting yourself fully, you protect your ability to save, invest, and build generational wealth. Inadequate financial protection is one of the greatest threats to a secure financial future.

| Scenario | With Adequate Coverage | With Underinsurance | With No Coverage |

|---|---|---|---|

| Major illness | Recover with manageable costs | Massive out-of-pocket debt | Total personal financial collapse |

| Home destroyed | Full rebuild, temporary housing covered | Partial rebuild, major shortfall | Complete loss, no assistance |

| Breadwinner death | Family stable, future secured | Years of financial struggle | Immediate hardship |

Useful Resources

To better understand insurance coverage limits and the true cost of underinsurance, explore these authoritative sources:

- Insurance Information Institute: Understanding Underinsurance – Official explanation of underinsurance risks across different policy types.

- Investopedia: Underinsurance Definition – Financial definition, examples, and strategies to avoid coverage gaps.

Frequently Asked Questions About Underinsurance Can Be More Dangerous

What is underinsurance?

Underinsurance means your insurance policy limits are too low to fully cover the actual cost of a loss or claim, leaving you financially responsible for the difference.

Why can underinsurance be more dangerous than no insurance?

Underinsurance Can Be More Dangerous because it creates a false sense of financial security, causing you to rely on protection that fails when you need it most, while still paying premiums.

How do I know if my coverage is insufficient?

Compare your policy limits to the replacement cost of your assets, your income, and your liabilities. If you cannot fully replace what is at risk, you likely have insurance gaps.

What are the biggest insurance mistakes people make?

Common insurance mistakes include buying minimum coverage, ignoring inflation, failing to review policies annually, and assuming employer insurance is enough.

How does inflation affect life insurance coverage?

Inflation impact insurance planning by reducing the real value of fixed death benefits over time. A policy that seems adequate today may leave dependents short in ten or twenty years.

What are the risks of insufficient coverage during emergencies?

Risks of insufficient coverage emergency situations include exhausting policy limits quickly, facing massive out-of-pocket expenses, and discovering excluded or capped coverage for critical needs.

Can underinsurance affect my health insurance?

Yes. Health insurance coverage gaps medical debt is a leading cause of bankruptcy. Low annual maximums and high deductibles leave patients with huge bills even after insurance pays.

How does property insurance replacement shortfall happen?

Property insurance replacement shortfall occurs when your policy covers market value but not the full cost to rebuild, which often rises due to construction and material price increases.

What is minimum coverage vs adequate coverage ?

Minimum coverage vs adequate coverage is the difference between meeting legal requirements and actually protecting your financial life. Adequate coverage matches your personal risk profile.

How often should I review my insurance policies?

You should review insurance coverage regularly, at least once per year or after any major life change like marriage, childbirth, home purchase, or job change.

Why do some people stay underinsured despite knowing the risks?

Behavioral biases such as optimism bias, present bias, and loss aversion lead people to underestimate risks and prioritize lower premiums over comprehensive financial protection.

What is a comprehensive risk assessment insurance plan?

A comprehensive risk assessment insurance plan evaluates all your assets, liabilities, income, and future needs to determine exact coverage amounts for every type of risk.

How does employer-provided insurance contribute to underinsurance?

Employer-provided insurance often has insurance gaps because it is designed as a basic benefit with lower limits and no personalization, leaving employees exposed to major risks.

Can underinsurance affect my family’s financial future?

Absolutely. Underinsurance life insurance dependents can face years of financial instability if policy payouts are too low to cover lost income, education, and daily living expenses.

What role do deductibles play in underinsurance?

High deductibles increase the likelihood of insurance gaps because you must pay a large amount before coverage kicks in, effectively making your policy useless for smaller claims.

Is partial insurance better than no insurance?

Not always. While partial coverage is better for small claims, underinsurance more dangerous than no coverage applies when the gap between coverage and actual cost leads to financial catastrophe.

What are examples of insurance gaps in home policies?

Common insurance gaps include exclusions for floods, earthquakes, and sewer backups, as well as sub-limits on jewelry, art, and temporary housing expenses.

How can I avoid the false sense of security from insurance?

Actively review insurance coverage regularly and perform a comprehensive risk assessment insurance check. Never assume your policy covers everything without reading the fine print.

What is the best strategy for insurance planning in 2025?

Start with a thorough financial planning review, buy policies with built-in inflation protection, and schedule annual insurance review meetings to adjust coverage as your life and costs change.

Should I buy additional insurance beyond employer coverage?

Yes. Most experts recommend supplementing employer insurance with individual policies to close insurance gaps and ensure your financial security is not tied solely to your job.